Discover the ultimate living alone financial safety checklist for adults 50+. Protect your finances, health, and independence with expert tips!

TL;DR

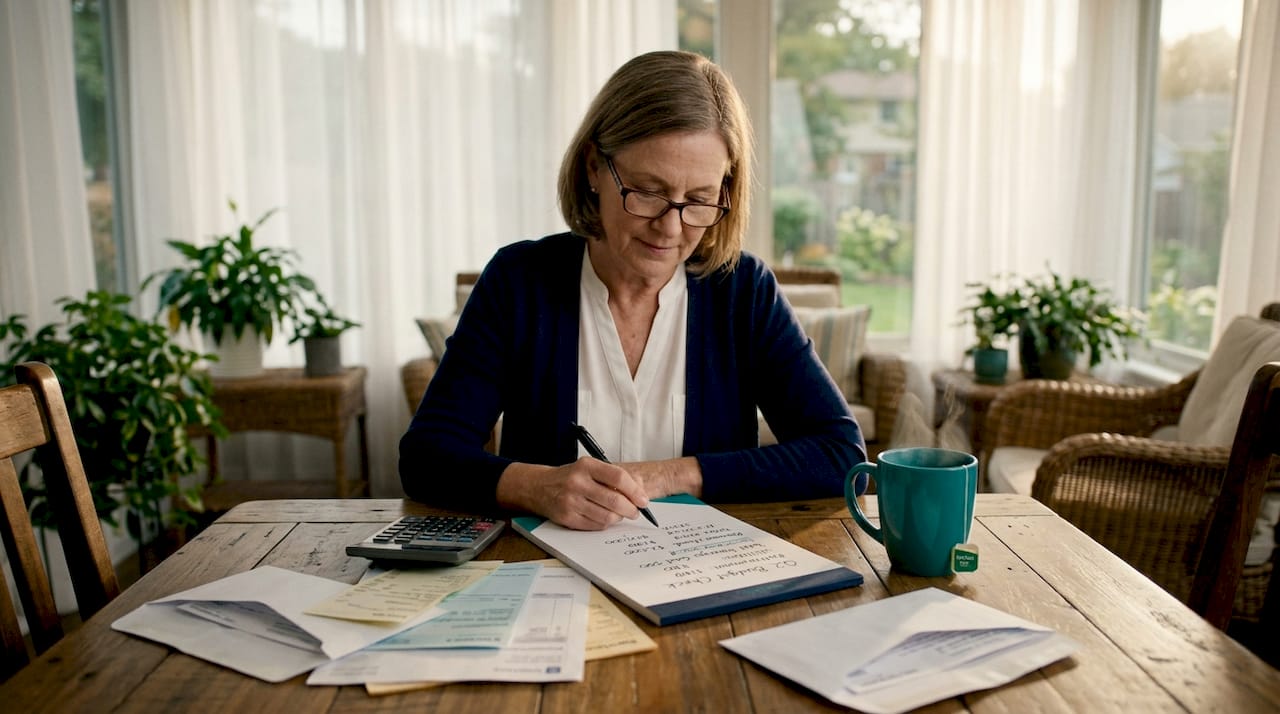

Living alone brings a unique kind of financial freedom. You make your own decisions, manage your own priorities, and answer to no one. But it also means there is no built-in backup when a bill is missed, a scammer calls, or an unexpected expense appears. Financial safety for solo agers isn't about having more money. It's about creating systems that help protect the life you've built.

This article walks through the core elements of personal financial safety for solo living: budgeting on a single income, building an emergency fund, organizing your documents, recognizing scams, and locking down your digital accounts. Each step is practical, specific, and designed to help you stay independent longer.

When you live alone, financial mistakes often stay hidden longer. There is no spouse noticing a suspicious charge, a missed payment, or an unusual withdrawal. That's why simple systems matter more than complex financial strategies.

A single-income budget is the foundation of every other item on this checklist. Without one, you cannot know whether your spending is sustainable or where your vulnerabilities are. Financial planning for singles from Fidelity makes clear that tracking spending carefully and building daily money management routines reduces both financial risk and decision fatigue over time.

Start by separating your costs into two categories:

Once you see both columns clearly, you can identify where money is leaving quietly and where you have room to redirect it toward savings or protection.

Tracking does not need to be complicated. A simple notebook, a spreadsheet, or an app like Mint or YNAB works well. The goal is consistency, not perfection. Reviewing your spending once a week for 15 minutes builds a habit that pays off when an unexpected cost arrives.

Pro Tip: If you find apps overwhelming, try a single-page expense journal. Write down every purchase for 30 days. Most people are surprised by two or three categories they had completely underestimated.

An emergency fund is not a luxury. It is the buffer between a bad month and a financial crisis. Research shows that 58% of adults living alone cannot handle an unexpected bill of around $1,000. That's exactly why even a modest emergency fund can create meaningful peace of mind — and why the margin matters so much for solo households.

The right target for your emergency fund is based on your own fixed monthly costs, not a generic rule. Here is a simple way to calculate it:

Consistent small deposits build real financial resilience over time, even when the starting amount feels modest. The habit matters as much as the balance.

Pro Tip: A high-yield savings account at an online bank like Ally or Marcus by Goldman Sachs typically offers better interest rates than traditional bank savings accounts, which means your emergency fund grows faster without any extra effort.

Delays in accessing financial information during emergencies create serious problems for solo adults. If you are hospitalized or incapacitated, the people trying to help you need to find your accounts, insurance policies, and passwords quickly. Creating an asset and bill access binder — or its encrypted digital equivalent — is one of the most protective steps you can take. Our Legal & Financial Basics guide walks you through this in detail.

Your document inventory should include:

"Maintaining an up-to-date, comprehensive financial and document inventory reduces emergency stress and ensures timely access to resources during health or financial crises." — Asset access and emergency preparation guidance

Store a physical copy in a fireproof box at home and a digital copy in an encrypted file or a secure cloud service like LastPass or 1Password. Tell one trusted person where to find it. Review and update the inventory every year, or after any major life change.

Our aging in place guide also recommends stress-testing your retirement funds and planning for home modification costs as part of this broader asset review. That is worth adding to your annual update.

Older adults lost over $3 billion to fraud in 2025. That figure represents real people who lost savings they cannot easily replace. Living alone increases your exposure because there is no second person to say, "Wait, does that seem right to you?"

The FTC's 2026 consumer data shows that scammers reach older adults primarily through text messages, phone calls, and social media. Common schemes include fake Medicare or Social Security alerts, grandparent scams, tech support fraud, and romance scams that build over weeks before requesting money.

Your fraud prevention checklist:

Prompt reporting and deletion of suspicious contacts reduces your exposure before a loss occurs. Prevention starts with recognizing the contact, not after money has moved.

Outdated passwords and unsecured devices are open doors. Changing all passwords for financial apps, your home Wi-Fi router, and any connected security devices after a move or major life change is a direct way to close those doors. For solo agers, digital security is a key part of maintaining independence — and it's simpler to set up than most people expect.

Here is what to update and when:

For managing all of this, a password manager designed for ease of use, such as Dashlane or Bitwarden, stores your credentials securely and generates strong passwords for you. You only need to remember one master password.

Pro Tip: Enable two-factor authentication on your bank accounts and email. This means even if someone gets your password, they still cannot log in without a code sent to your phone.

Agingsolo's guide on technology for aging solo covers additional tools that support both financial safety and daily independence for solo adults.

Staying in your home as you age is the goal for most solo adults. But the financial planning required to make that work goes beyond monthly budgeting. It includes anticipating costs that do not exist yet.

Home modifications like grab bars, ramp installations, or stair lifts can cost anywhere from a few hundred to several thousand dollars. In-home care, even part-time, adds a recurring expense that most people have not factored into their retirement projections. The Splitero aging-in-place checklist recommends calculating these costs now and building them into your long-term financial plan before they become urgent.

Review your health insurance and long-term care coverage as part of this process. If you do not have long-term care insurance, look at what your state's Medicaid program covers and at what income level. Knowing the threshold now gives you time to plan around it. The legal and financial basics guide from Agingsolo covers wills, power of attorney, and related planning in plain language.

A living alone financial safety checklist works because it addresses the specific vulnerabilities of solo adults: no shared income, no built-in second opinion, and no automatic backup when something goes wrong.

| Point | Details |

|---|---|

| Budget on a single income | Separate fixed and discretionary costs, then track spending weekly to stay in control. |

| Size your emergency fund correctly | Base your target on your actual fixed monthly costs, not a generic number. |

| Organize your documents now | Keep an updated asset and bill access inventory so trusted contacts can help in a crisis. |

| Prevent fraud proactively | Set up credit bureau alerts, add a trusted contact to accounts, and report suspicious contacts immediately. |

| Secure your technology | Update passwords on financial apps, Wi-Fi, and smart devices after any major life change. |

I've talked with a lot of solo agers over the years, and the pattern I see most often is this: people are good at handling the big, visible financial decisions. They manage their retirement accounts. They pay their bills on time. What catches them off guard is the quiet accumulation of small vulnerabilities.

The fraud call that comes on a tired Tuesday afternoon. The password that hasn't been changed since 2019. The emergency fund that was never quite built because there was always something else to spend it on. These are not failures of intelligence. They are the natural result of carrying everything alone, without a second set of eyes.

What I've found actually works is treating this checklist not as a one-time project but as a living practice. Review your budget quarterly. Update your document binder once a year. Check your credit report every four months using AnnualCreditReport.com. These small, regular habits do more for your financial safety than any single large action.

The emotional side of this matters too. Managing finances alone carries a cognitive weight that people rarely talk about. Every decision lands on you. Building a small team around you, a financial advisor, a trusted friend, an accountant, reduces that weight and reduces your risk at the same time. You do not have to do this entirely solo.

— Mike

Financial safety isn't really about money. It's about preserving choices. The stronger your financial foundation becomes, the more freedom you have to remain independent, stay in your home, and make decisions on your own terms.

Bookmark this checklist and run through it once a year — or after any major life change. These small habits keep your financial safety net strong.

If this checklist has surfaced questions you are not sure how to answer, you are not alone in that. Agingsolo exists specifically for people in your position: adults over 50 who are building a safe, independent life without a built-in support system.

The aging in place guide covers budgeting, home safety, and long-term financial planning in one place. If you want to think through who would help you in a crisis, the support circle builder walks you through identifying and organizing the people you trust. And if you want to stay connected with others navigating the same path, the community groups resource explains how peer groups reduce both financial and emotional risk for solo agers. Agingsolo's tools are calm, practical, and built for exactly where you are.